The Next Phase of AnomIQ: Advanced Structural Market Analytics

🚀 UPDATE [March 11, 2026]: The architectural updates detailed below are now live in production! > We have completely rebuilt the diagnostic terminal to visualize Market Friction, Net Taker Imbalance, and Volume Anomalies. 👉 Read the Deep Dive 2.0 Launch Announcement and see the new dashboard here.

Since our launch, AnomIQ’s real-time engine has focused on a singular goal: detecting statistically significant volume and volatility anomalies the second they occur.

However, in professional data analysis, detecting an anomaly is only the beginning. Once a statistical deviation is flagged, the next objective is understanding the underlying data structure. Is the data flow indicating a new directional trend, or is it encountering passive liquidity absorption?

To help our users diagnose these complex market states, our engineering team is finalizing a major architectural expansion of our data suite.

We are currently developing a new suite of structural metrics for the Deep Dive dashboard. This update transitions AnomIQ from a detection-focused tool to a comprehensive diagnostic terminal for digital asset market physics.

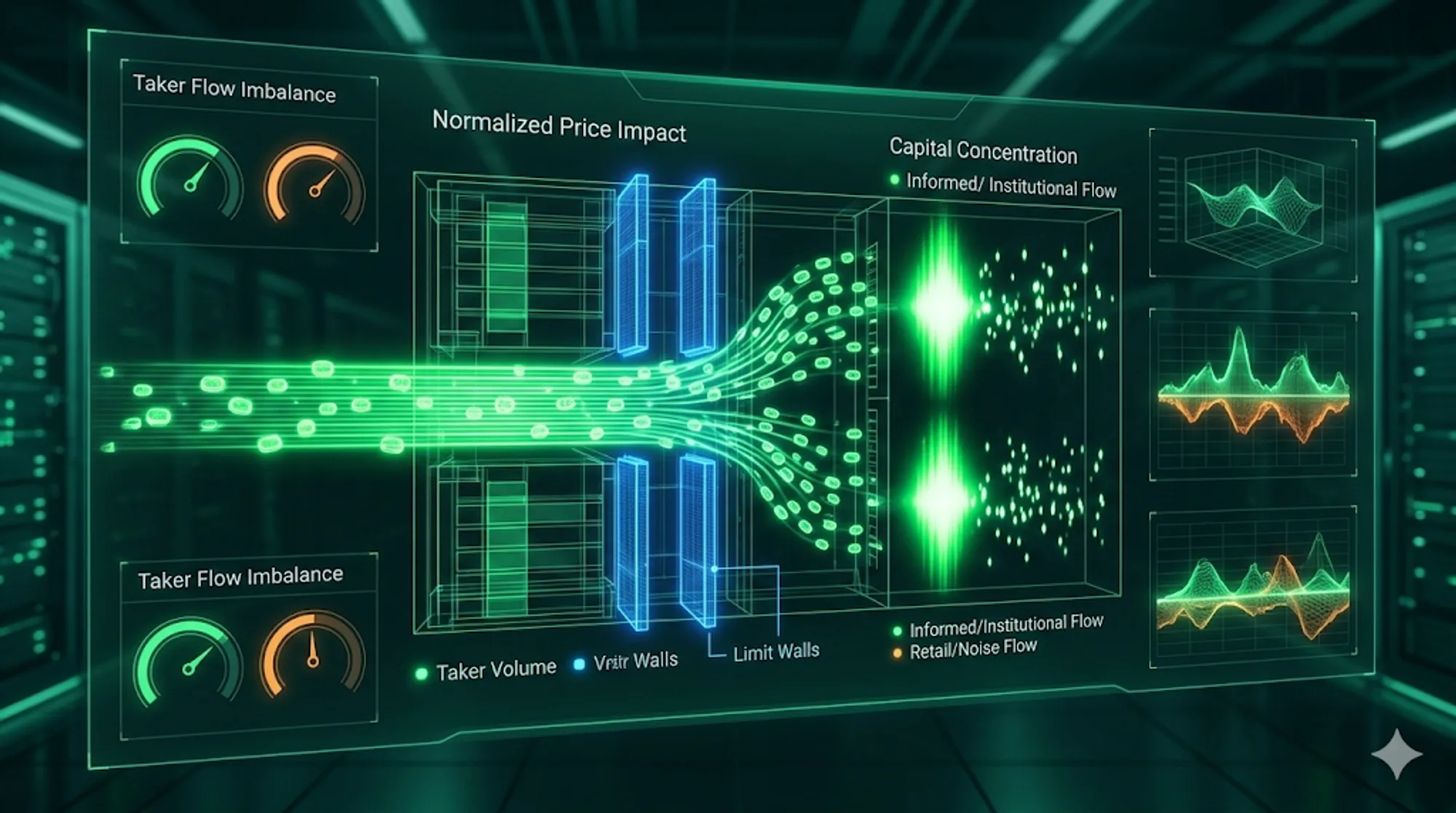

1. Measuring Liquidity Resilience: Normalized Impact Score

Evaluating the “thickness” of an order book is essential for understanding market stability. However, applying static dollar amounts is an outdated approach in digital asset markets where volume profiles fluctuate wildly.

To solve this, we are developing a Normalized Impact metric. Instead of fixed currency values, it calculates price movement relative to an asset’s historical volume baseline for that specific time of day.

The Analytical Insight: This metric allows users to identify when high relative volume yields minimal price movement—a state known as “Passive Absorption.” It helps data analysts identify where massive liquidity layers are absorbing market participation, providing a clearer picture of market support and resistance.

2. Participation Profiling: Capital Concentration

Not all volume has the same structural footprint. By calculating the statistical Z-scores of Total Volume against Event Frequency, we will soon be able to mathematically profile the nature of the participants driving the data.

The Analytical Insight: Users can identify the structural divergence between fragmented, high-frequency liquidity (retail participation) and concentrated, high-conviction positioning. By utilizing our Capital Concentration Score, analysts can measure the density of order flow through a purely mathematical lens. This eliminates the need for subjective labels and focuses the analysis on large-scale structural actors.

3. Directional Flow Imbalance

While Z-scores are excellent for anomaly detection, understanding structural trends requires observing raw data flow. Therefore, our team is integrating absolute liquidity metrics for aggressive execution.

The Analytical Insight: Instead of just aggregate volume, you will be able to dissect the balance between buyer-initiated and seller-initiated flow. Our planned Flow Imbalance metric provides an instant, normalized read on which side of the market is currently dominating the execution tape.

Upcoming Diagnostic Visualizations

Raw data is only useful if it can be interpreted at the speed of the market. To ensure these new metrics are immediately accessible, we are actively designing dedicated visual components:

- Absorption Modules: Real-time maps that contrast Volume against Price Impact to highlight liquidity walls.

- Participation Divergence: Comparative indicators that contrast buy-side and sell-side concentration scores to highlight structural shifts.

Release Timeline

We will publish an official technical brief here on the blog the moment these infrastructure updates are available.